Rule of 40: Use It Before You Spend, Not After

Revenue growth rate plus EBITDA margin. If the sum hits 40%, you're in healthy territory. That's the Rule of 40, and it's been the shorthand benchmark for SaaS financial health since Brad Feld coined it a decade ago.

Here's the thing, though. Most finance teams I've worked with calculate it after the quarter closes, drop it into a board deck, and move on. It's a report card. And report cards are fine, but they don't change the grade.

The real value is running it forward. Before you lock in next quarter's hiring plan, before you approve a pricing change, before the board signs off on the budget, check the math. What does this decision do to the score? Because the valuation gap between companies that clear 40% and companies that don't is massive, and it's getting wider.

I've been using the Rule of 40 with clients for about two years now. Maybe half of them are already aware of it when we start working together, but even the ones who know the concept aren't usually tracking it in any structured way. I introduce it because the valuation impact is significant, and it gives us a framework to define which initiatives are worth taking on and what kind of returns they need to generate.

The Numbers Are Pretty Clear

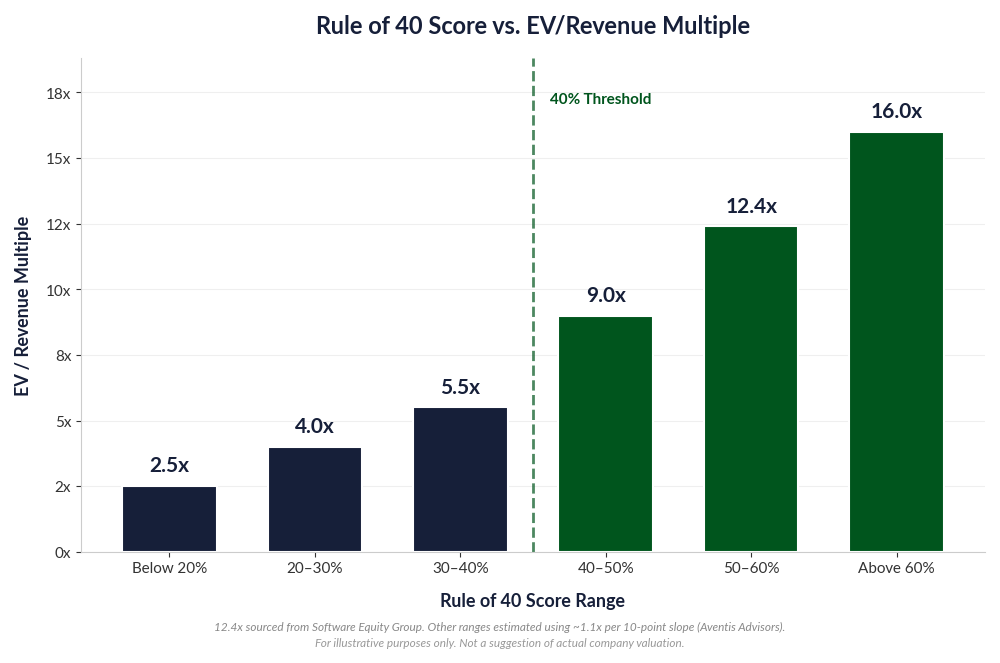

Out of actively traded public SaaS companies, only about 17% exceed the Rule of 40. The median score sits around 23%, down from roughly 30% back in 2015. So the bar hasn't gotten easier to clear. It's gotten harder.

The payoff for clearing it is real, though. Companies scoring above 40% on a weighted basis post a median EV/Revenue multiple of 12.4x. Companies that don't clear it? They're clustered down around 3x to 5x. And every 10-point improvement in your score corresponds to roughly +1.1x on your EV/Revenue multiple. On a $30M ARR business, moving from a 25% score to a 45% score could mean $60M or more in additional enterprise value, and potentially multiples of that if the higher score pushes you past the 40% threshold where buyer premiums really kick in.

Companies scoring above 60% (think CrowdStrike, Datadog in their peak years) trade at a fundamentally different level than the median. That's not a rounding error. It changes the entire conversation with investors, acquirers, or your board.

Most Teams Calculate It Wrong (Or Not Usefully)

The formula itself is simple. Revenue growth % + EBITDA margin % = Rule of 40 score. But there are a few decisions baked into that calculation that change the answer significantly.

Which growth rate? Trailing twelve months is the standard, but if you're planning forward, you want the projected growth rate for the next four quarters. Use year-over-year to smooth out seasonality. If you only look at quarter-over-quarter, one strong Q4 can make a mediocre year look great.

Which margin? EBITDA is the most common, but some investors prefer free cash flow margin. For middle market SaaS companies, EBITDA margin is cleaner because it strips out the noise from capex timing and working capital swings. If your acquirer or investor uses FCF margin, know the difference and be ready to show both.

What's the right time horizon? I'd use at least a trailing six-month window for the margin component, and ideally twelve months — the same period over which you're measuring revenue growth. That consistency matters. Monthly margins bounce around too much, especially if you're a $10M to $50M company with lumpy professional services revenue or annual contract renewals concentrated in Q4.

Running It Forward: A Practical Example

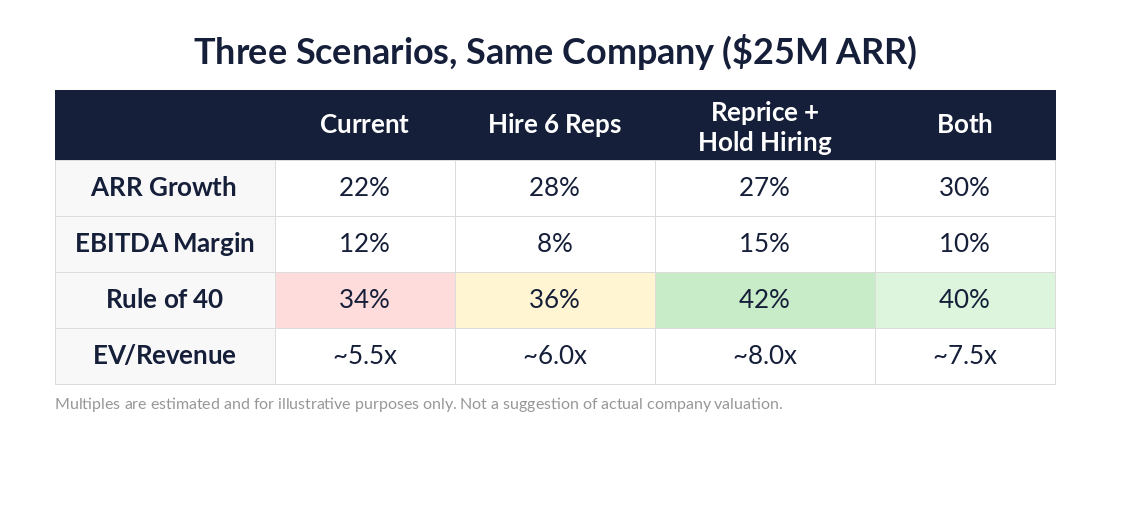

Let's say you're a $25M ARR SaaS company growing at 22% with a 12% EBITDA margin. That puts you at a 34% Rule of 40 score. Not bad, but below the threshold.

Your VP of Sales wants to hire six reps in Q2. Loaded cost: $900K for the year, with pipeline impact starting in Q3. Your VP of Product wants to ship a new pricing tier that bumps ARPU 8% but risks a 2-3 point hit to gross retention during the transition.

Before either of those gets approved, run the Rule of 40 forward.

Scenario A: Hire the reps, hold pricing. Growth accelerates to 28% by Q4 as the new reps ramp (assuming a 6-month ramp to quota). But the added headcount drags EBITDA margin to 8%. New score: 36%. You moved sideways.

Scenario B: Hold hiring, change pricing. Growth jumps to 27%. If the pricing change sticks and retention holds, EBITDA margin climbs to 15% as ARPU flows through. Score: 42%. Estimated multiple jumps to ~8.0x. That one change got you across the line.

Scenario C: Do both. This is the one that surprises people. Growth hits 30% as ARPU increases and the new hires drive some additional revenue late in the year, but margin only lands at 10% due to all the incremental costs. Score: 40%, estimated multiple ~7.5x.

What this example doesn’t look at is how the EBITDA margin changes in year 2 after the six new hires have ramped and are producing at what we can assume would be an average level. This may change the decision, so the timelines you’re evaluating these decisions based on become important as well.

Nobody runs these three scenarios side by side. The sales team builds a pipeline model to justify the hires. The product team builds a revenue model to justify the pricing change. And the CFO finds out at the board meeting that the two decisions, taken together, moved the Rule of 40 score three points less than the optimal decision.

This kind of scenario analysis is exactly where most planning conversations go sideways. Each department builds its own business case in isolation, and the CFO ends up reconciling competing models after the decisions are already half-made. Running the Rule of 40 forward forces the tradeoffs into the open before anyone's committed.

Building It Into Your Planning Model

If you want Rule of 40 to be a planning input rather than a reporting output, it needs to live in your operating model. Here's what that looks like in practice.

Add a Rule of 40 row to your monthly forecast. Not just the trailing calculation, but the forward-looking version that uses your projected growth rate and margin targets. Color-code it: green above 40%, yellow at 30-39%, red below 30%. It sounds simple, but I've seen plenty of $20M+ SaaS companies that don't have this anywhere in their reporting package.

Run sensitivity analysis on the two inputs separately. Most companies have more control over margin than growth in the short term. If you're at 35% and need to get to 40%, map out whether it's easier to add 5 points of growth or 5 points of margin. Usually it's margin, because you can cut or defer spend in 30 days. Growth takes quarters.

Test every major spend decision against it. New headcount, new tooling, a market expansion, a price change. Pull the Rule of 40 score for each scenario and put it in the board memo alongside the NPV or payback period. It takes ten minutes if the model is built right, and it frames the decision in terms that investors and acquirers immediately understand. (If you're curious what a structured planning process looks like for this kind of work, that's essentially what we do.)

When we build this into a client's model, the reaction is less surprised and more informed. Most of these teams know their margins are tight or their growth is slowing, but they haven't been tracking the combined score. Once it's visible, it becomes a guiding light. It helps the organization focus on becoming leaner (cost-out initiatives, efficiency improvements) instead of chasing distractions that don't actually drive enterprise value.

Where This Matters Most

The Rule of 40 isn't just a SaaS metric anymore. PE firms and strategic acquirers use it (or a close variant) to screen middle market deals across recurring revenue businesses. If you're anywhere near a transaction, whether that's 6 months away or 3 years away, your Rule of 40 trend line is part of the story a buyer will build about your company.

Companies clearing the threshold consistently command a 121% valuation premium over those that don't. That gap is too big to discover after the budget is already committed.

Score it before you spend. Not after.

If your planning model doesn't include a forward-looking Rule of 40 calculation yet, that's a quick win.