Hidden Operational Risks in Scaling: 5 Questions Your Finance Team Must Answer

The $15M+ Scaling Trap: Why Revenue Hides Risk

Growth is a powerful sedative. When top-line revenue is compounding at 30% or 40% annually, it is easy to ignore the creaks in the floorboards. Inefficiencies in customer acquisition, slight dips in retention, or ballooning general and administrative costs are masked by the influx of new cash. But as you cross the $15M ARR threshold, the physics of your business change. The law of large numbers takes hold. Growth slows naturally, and suddenly, those inefficiencies are no longer rounding errors. They are valuation killers.

According to Gartner, scale-focused companies that prioritize operational productivity achieve 10.6% higher performance than their rivals. The inverse is also true: companies that scale without a rigorous operating architecture do not just stagnate; they bleed.

Most executives in the $15M to $50M revenue band believe they are managing the business well because they hit their sales targets. However, if you are managing by your bank balance or your "gut" feeling, you have already lost control of your margins. You are likely stuck in what industry data calls "No-Man's Land", too big to be nimble, but too unstructured to be efficient.

This article outlines the specific hidden risks that emerge during this critical scaling phase. We will examine the five diagnostic questions you must ask your finance team immediately. These are not questions about accounting compliance. They are questions about the Foundational Operating Model that dictates whether you are building an enterprise or just running a really large small business.

Question 1: Can you produce an accurate P&L and Balance Sheet within 20 days of month-end?

Speed is a proxy for accuracy and process maturity.

If your finance team takes 45 days to close the books, you are looking at data that is nearly two months old. In a recurring revenue business, a two-month lag is an eternity. You cannot pivot marketing spend, adjust hiring plans, or intervene in churn risks based on data from last quarter.

A slow close indicates that your financial data is being manually assembled rather than systematically generated. This manual intervention introduces error risk and consumes valuable time that should be spent on analysis.

If the answer is "No," your business needs a bookkeeper to fix the past, not a strategic partner to model the future. You are operating with a rearview mirror that is fogged up. You need an efficient accounting function where data ingestion is automated, and the close process is a non-event. This allows your VP of Finance or CFO to spend the first week of the month analyzing why the numbers occurred, rather than verifying if the numbers are correct.

You must produce a Flash Report by Day 5 and a full monthly close by Day 20. If your organization cannot meet these deadlines, your core accounting processes are broken. You must stabilize your financial data and reporting cycles before you can implement a strategic FP&A function.

Question 2: Can you show leadership exactly how a 1% change in lead conversion or churn will impact cash in 6 months?

Most finance teams can tell you what your churn was last month. Very few can tell you what a 1% increase in churn today will do to your cash runway in December. This inability to connect operational drivers (leads, conversion rates, usage metrics) to financial outcomes (revenue, cash, EBITDA) is a massive blind spot.

When you decouple operations from finance, department heads operate in silos. Marketing celebrates a lower Cost Per Lead (CPL), but Finance realizes those cheap leads are churning at double the rate. Sales celebrates hitting quota, but Professional Services is drowning because the deals sold have negative gross margins.

This question validates the presence of a Foundational Operating Model. It tests whether your financial model is a static spreadsheet or a dynamic simulation of your business.

Strategic leadership requires connecting operational "drivers" directly to the bottom line. You must be able to toggle a variable in your model, such as increasing customer acquisition costs by 3%, and see the immediate impact on profitability and cash flow. This is the kind of strategic financial analysis our Foundational Operating Model enables. It moves you from reactive reporting to proactive management.

Question 3: Do your monthly leadership meetings spend more time debating if the numbers are right than deciding what to do about them?

We see this constantly. The Monthly Business Review (MBR) begins. The VP of Sales says, "My dashboard shows $2.1M in bookings." The CFO says, "The P&L only shows $1.9M recognized." The next 45 minutes are spent arguing over definitions, timing, and data sources. The strategy session dies on the table.

This is a failure of the "Single Source of Truth." If your executives do not trust the data, they will continue to make decisions based on gut instinct. You are paying high salaries for smart people to argue about arithmetic.

This question tests for executive alignment and data integrity. If you are still validating data, you are not executing strategy; you are stuck in a backward-looking reporting cycle. A mature Monthly Strategic Session trusts that the numbers are correct. The agenda should focus entirely on forward-looking decisions: "Given that we are $200k behind on bookings but ahead on pipeline, do we pull forward the Q3 hiring plan?"

Question 4: Do you have a math-based hierarchy that ranks your growth opportunities by ROI?

Your Head of Product wants to launch a new module. Your Head of Sales wants to open a London office. Your Head of Marketing wants to sponsor a Tier 1 conference. You cannot do all three. How do you choose?

In most $15M+ firms, the decision is made based on who argues the loudest or which initiative "feels" most strategic. This is capital allocation by charisma, and it is dangerous.

Without a standardized framework for Capital Allocation, you will inevitably misallocate resources. You might invest $500k in a new product line that yields a 10% return, while starving a marketing channel that was generating a 400% return.

Without a math-based hierarchy, the CEO is relying on "gut" or "bank statements," which is high-risk at the $20M+ enterprise level. You need a unified ROI framework. Every capital request must be accompanied by a projected payback period, NPV, and IRR or ROI.

Your finance team should present a ranked list of investments every quarter, sorted by:

1. Certainty of Return (Low/Med/High)

2. Payback Period (Months)

3. Net Present Value

4. IRR or ROI (%)

3. Strategic Alignment (Score 1-5)

This removes emotion from the boardroom and refocuses the team on efficient growth.

Question 5: If you hired a full-time CFO tomorrow, would they spend their first 90 days building your financial systems or driving your growth?

Many CEOs delay hiring a true strategic finance leader because they "aren't big enough yet." When they finally do hire a CFO (usually around $25M-$40M ARR), that expensive executive spends their first six months cleaning up messy data, implementing an ERP, and firing or training up underperforming bookkeepers.

You are paying a strategic price for tactical work. You do not hire a race car driver to build the engine; you hire them to drive the car. If your infrastructure is not ready, your new CFO will be handcuffed.

High-growth companies need to implement the processes and build the rhythms and accountability now so that future executive hires can hit the ground running. By installing a robust Foundational Operating Model at $15M ARR, you ensure that when you eventually bring in the heavy hitters, they can immediately focus on the high-value initiatives that will drive growth like M&A, fundraising, and market expansion.

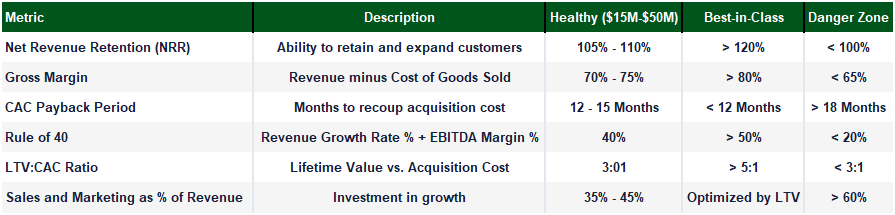

Benchmarks: The Math of Scaling

To operate at the enterprise level, you must measure yourself against enterprise standards. The following benchmarks are critical for B2B recurring revenue firms between $15M and $50M ARR. These are not targets; they are the floor for high-performance scaling.

Critical KPI Formulas

1. Customer Lifetime Value (LTV)

Do not use revenue. Use Gross Margin. Revenue LTV overstates the value of a customer by ignoring the cost to serve them.

LTV = (Average Revenue Per Account x Gross Margin) / Churn Rate

2. CAC Payback Period

This is your cash flow risk metric. It tells you how long you are financing a new customer before they become profitable.

CAC Payback = Customer Acquisition Cost / (Average Monthly Revenue x Gross Margin %)

3. Net Revenue Retention (NRR)

The ultimate measure of product-market fit and customer health. This measures how much your existing customer base is growing or shrinking.

NRR = (Starting ARR + Expansion ARR - Contraction ARR - Churned ARR) / Starting ARR

4. The Rule of 40

The standard for balancing growth and profitability. This is a common metric utilized by investors in valuing businesses.

Rule of 40 = Annual Revenue Growth Rate % + EBITDA Margin %

Get Your Business Ready to Scale Quickly and Efficiently

Scaling from $5M to $15M is about product-market fit and sales hustle. Scaling from $15M to $50M is about operational rigor and capital efficiency. The risks at this stage are not always visible. They hide in the lag between a decision and its financial impact. They hide in the definitions of your KPIs. They hide in the manual spreadsheets your finance team is desperately trying to reconcile.

If you asked your finance team the five questions above and received hesitation, excuses, or blank stares, you are carrying operational risk that will suppress your valuation. You do not need more complexity; you need clarity. You need a financial infrastructure that supports your ambition rather than anchoring it.

It is time to stop managing by your bank balance. Build the model. Trust the math. Scale the business.

Ready to begin the shift to a forward-looking, strategic FP&A function with your customer Foundational Operating Model?